Top 11 Mortgage Myths To Be Aware Of When Buying A Home

Have questions about buying or selling a home?

Ask Now!What Are The Most Common Mortgage Myths?

Top 11 Mortgage Myths To Avoid When Buying A Home

One of the most important steps to buying a home is successfully obtaining financing, which is frequently done by getting a mortgage. The mortgage process can be relatively easy for home buyers who have an understanding of the process.

In addition to having an understanding of the mortgage process, it’s also important to be aware of potential myths that may exist. There are dozens of mortgage myths that exist and it’s important to not believe something that isn’t true.

In this article we’re going to discuss the top 11 mortgage myths that you need to be aware of when buying a home. Falling for one of the following myths can make the process of getting a mortgage a disaster.

1.) A Pre-Qualification & Pre-Approval Are The Same

Many home buyers believe that a pre-qualification and pre-approval are the same thing, which is one of the most common mortgage myths. There actually is significant difference between a mortgage pre-qualification and a mortgage pre-approval.

One of the biggest differences between a mortgage pre-qualification and pre-approval is the information that’s required.

In order to obtain a mortgage pre-qualification, a borrower provides information regarding their income, employment, and debts to a lender which is then used to determine the potential borrowers likelihood they could get a mortgage. The information that’s provided to a lender is typically not verified until the borrower applies for their mortgage so you can imagine the problems that can exist if a borrower provides false or incorrect information.

In order for a borrower to obtain a mortgage pre-approval, a lender is going to verify a borrowers credit, employment, income, and other financial information. This allows a mortgage lender to make a better prediction as to whether a borrower will actually get funding for a home purchase since the information is verified.

One of the worst mortgage mistakes made by home buyers is not obtaining a pre-approval and settling for a pre-qualification. A home buyer with a pre-approval gives themselves a significant advantage over buyers who settle for a mortgage pre-qualification should there be a multiple offer situation.

It’s critical that when buying a home you don’t believe that a pre-qualification and pre-approval are the same!

2.) Getting Pre-Approved Guarantees That You’ll Get A Home Loan

Top Mortgage Myths BUSTED! Getting Pre-Approved Doesn’t Guarantee You’ll Get A Home Loan!

There are thousands of horror stories of home buyers who’re approved for a mortgage only to find out at a later time they’ve been denied for their home loan. One of the top 11 mortgage myths is believing that once you’re pre-approved you’re guaranteed to get a home loan.

There are actually lots of reasons why a mortgage is denied after being approved. Some of the most common reasons include changing jobs, adding additional debts, and not having enough money to cover costs of getting the mortgage.

It’s important that once you’re pre-approved for a mortgage that you don’t make any rash decisions when it comes to your financials. If you’ve been pre-approved for a home loan and are thinking about making a financial change that you first consult with your mortgage professional to make sure you’re not sabotaging your pre-approval.

3.) A 20% Down Payment Is Required To Get A Mortgage

A common mortgage myth that exists is that only potential borrowers who have 20% or more to put towards a down payment can get a home loan. There certainly are some great mortgage products that reward borrowers who have 20% to use towards a down payment, however, it’s not necessary in order to get a mortgage.

An excellent tip for home buyers is to first determine which type of mortgage is best for their individual circumstances. There are mortgage products available for buyers who have down payment percentages ranging from 0% to 20% or more!

Many home buyers have a hard time that they can potentially buy a home with no money or very little. There are some fantastic mortgage products for those buyers who may not have much money saved.

It’s important to note however that there are PROs and CONs of buying a home with a small down payment. It’s recommended that potential home buyers discuss with an experienced mortgage broker or lender to see which option will be the best fit for them.

4.) Perfect Credit Is Needed To Get A Mortgage

Credit is very important when applying to get a mortgage to buy a home, however, one of the most common mortgage myths is that only borrowers with perfect credit can get a mortgage. If a potential borrower has a credit score of 450, getting a mortgage will be highly unlikely, but a potential borrower with a 600 credit score might still be able to obtain home financing.

Credit scores impact the interest rate a borrower is offered and also whether a borrower is approved for a loan, but an 800+ score isn’t necessary. There are many mortgage products that exist that’re tailored to help potential borrowers with 600-650 credit scores.

It’s obviously not recommended to strive for credit scores of 600-650, however, buyers who believe they don’t have perfect credit shouldn’t completely give up on the idea of getting a mortgage. If you believe you have below average or average credit, follow these helpful tips for improving credit scores to buy a home because you don’t need perfect credit to get a mortgage!

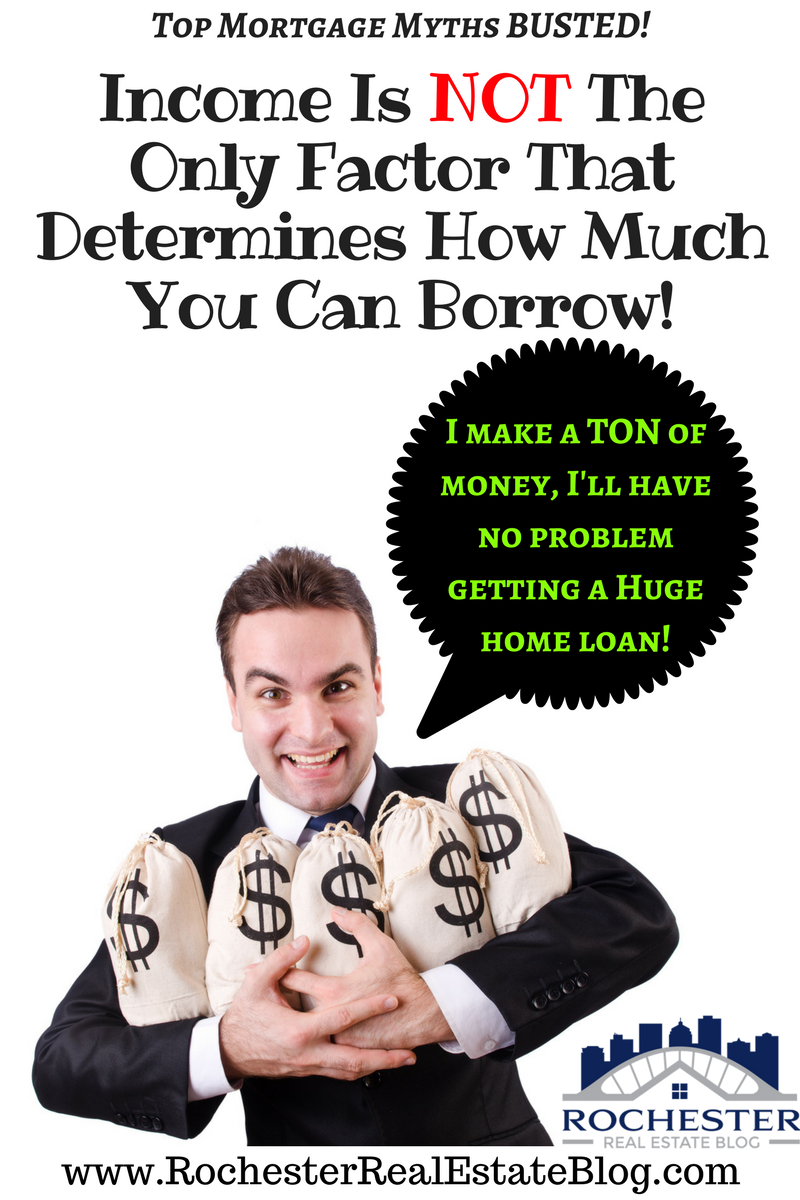

5.) Only Your Income Determines How Much You Can Borrow

Top Mortgage Myths BUSTED! Income Is NOT The Only Factor That Determines How Much You Can Borrow!

The amount of income a potential borrower makes is absolutely important, however, it’s not the only factor in determining how much they can actually borrow. One of the most frequently asked questions about mortgages relates to how much the borrower can actually spend on a home.

It’s not unusual to hear a potential buyer say, “I make $100,000 a year, how come I can’t buy a more expensive home?” Well, if a buyer makes $100,000 a year but has thousands of dollars in student loan debt, it’s going to impact the maximum price of a home they can purchase.

Debts, such as student loans impact how much you can borrow to buy a home for sure, especially with millennial home buyers. There are other factors as well such as credit scores and the down payment percentage. Income is only one piece of the puzzle when it comes to determining how much a home buyer can borrow.

6.) It’s Always Best To Get A 30 Year Mortgage

The thought process that mortgages with the longest term is always the best is another one of the top 11 mortgage myths. Many home buyers believe that getting a 30 year mortgage is the best but are potentially missing out on a better mortgage product.

Why in the world would a 15 year mortgage be better than a 30 year mortgage? While the monthly payment will be higher on a 15 year mortgage when comparing to a 30 year mortgage, the amount of total interest paid is significantly lower. Also, the amount of equity that a buyer has in their home grows faster with a 15 year mortgage than it will with a 30 year mortgage.

This is only one reason why a 30 year mortgage isn’t the best for some borrowers. 30 year mortgages are great for borrowers who haven’t saved money for down payment or who don’t have a lot of reserve money available, but it’s certainly not always best for everyone.

7.) All Mortgage Brokers & Lenders Are The Same

One of the most ridiculous myths in real estate is that all agents are the same. The myth that all mortgage brokers and lenders are the same is one of the top mortgage myths.

There are many things that differentiate mortgage brokers and lenders. First and foremost, there is a difference between a mortgage broker and a mortgage lender, which many buyers don’t even realize. Picking a mortgage company when buying a home is extremely important because they aren’t all the same.

Each and every mortgage broker and mortgage lender offers different mortgage products, charges different fees, offers different interest rates, and has different mortgage guidelines. It’s suggested when buying a home that you look into a few different mortgage companies to make sure you’re getting the best mortgage for your individual circumstance. An experienced real estate agent will also be able to explain why they’ve used certain mortgage lenders in the past and provide a few suggestions to make sure you’re using a solid company.

8.) FHA Home Loans Are For Borrowers With No Money & Poor Credit

One of the most popular mortgage products is the FHA home loan. The FHA home loan, which is a loan insured by the Federal Housing Administration, and is very popular among first time home buyers.

The belief that FHA home loans are only for borrowers with no money and poor credit is another common mortgage myth. Like with anything, there are positives and negatives of FHA mortgages.

FHA home loans are definitely a great option for borrowers who don’t have a significant down payment and lower credit, but that doesn’t mean that only borrowers that fit that criteria take advantage of FHA home loans. The FHA home loan interest rates are often the lowest available for borrowers, which is a reason why a borrower with great credit and money available would take advantage of an FHA loan.

9.) If You’re Denied For A Mortgage Once You’ll Never Be Able To Get A Mortgage

If You’re Denied For A Mortgage You CAN Get Approved In The Future!

Many potential buyers believe that once they’ve been denied for a mortgage, they’ll never be able to get a mortgage again. This is another popular mortgage myth that exists and often discourages potential buyers from working towards getting a mortgage in the future.

If you happened to be turned down when applying for a mortgage, don’t fret. By following the proper step by step directions to getting a mortgage after being denied, you CAN get a mortgage in the future!

Tips such as paying off debts, paying bills on time, and improving credit scores can help work towards the ultimate goal of securing a mortgage if you’ve been turned down in the past. It’s important that you don’t get discouraged after being turned down for a loan and fall for this common mortgage myth because it is possible.

10.) Paying Off A Mortgage As Quick As Possible Is Always Best

There aren’t many people who enjoy being up to their eyeballs in debt and certainly a mortgage is one of the top debts someone can have. It makes sense to pay off a mortgage as quick as possible than, right?

Paying off a mortgage as quick as possible is actually not always the best idea, which makes it another popular mortgage myth. Mortgage interest rates have remained low for several years now, so it’s very possible there are better debts to pay off before a mortgage.

For example, if you had a personal loan of $50,000 at an interest rate of 10% and a mortgage loan of $50,000 at an interest rate of 3.5%, it makes more sense to pay off the loan with the higher interest rate.

11.) After a Bankruptcy, Judgments, Or Collections You’ll Never Be Able To Get A Mortgage

It’s unfortunate when people have a bankruptcy or to have a bunch of judgments filed against them. Another one of the most common mortgage myths that exists is that after a bankruptcy, judgments, or collections are filled against someone that they’ll never be able to get a mortgage again.

Depending on whether a bankruptcy is a Chapter 7 or 11, there are a minimum number of years that must pass before you’d able to secure mortgage financing. It’s important that if you do have a bankruptcy or judgments that you discuss with an experienced mortgage consultant about the steps to take to secure financing in the future.

Final Thoughts

As you’re preparing to get a mortgage to buy a home, it’s vital that you don’t fall for any of the above mortgage myths. Believing these crazy myths can make the mortgage process a miserable one.

If you happen to hear something relating to mortgages that seems a little crazy, ask an experienced mortgage consultant or real estate agent. They should be able to help you identify whether or not what you’ve heard is just another mortgage myth or if it’s a fact.

Other Helpful Home Financing & Mortgage Resources

- Facts About VA Home Loans via Bill Gassett

- Why Do Real Estate Agents Ask For Mortgage Pre-Approvals

- Is An Adjustable Rate Mortgage A Good Idea via Dan Barcelon

If you’re thinking about buying a home in Rochester NY, make sure that you’re aware of the above mortgage myths. These mortgage myths often leave potential buyers believing they have no chance at getting a home loan. If you aren’t working with a top Rochester NY real estate agent, contact me so that we can discuss your home buying situation!

About the authors: The above article “Top 11 Mortgage Myths To Be Aware Of When Buying A Home” was written by Kyle Hiscock of the Hiscock Sold Team at RE/MAX Realty Group. With over 35 years combined experience, if you’re thinking of selling or buying, we’d love to share our knowledge and expertise.

We service the following Greater Rochester NY areas: Irondequoit, Webster, Penfield, Pittsford, Fairport, Brighton, Greece, Gates, Hilton, Brockport, Mendon, Henrietta, Perinton, Churchville, Scottsville, East Rochester, Rush, Honeoye Falls, Chili, and Victor NY.