Top Mortgage Myths | Demystifying Common Home Loan Misconceptions

Have questions about buying or selling a home?

Ask Now!

No one ever said that getting approved for a mortgage would be easy, but that doesn’t mean it’s impossible, even for those would-be buyers who are afraid that they won’t qualify for a home loan.

The truth is, there are many paths to home ownership, some of which you might not be aware of without the guidance of a mortgage industry expert.

That’s why we’re here to dispel some of the most common misconceptions of home loans, as well as offer some friendly advice as you begin your journey to becoming a homeowner.

“Paying for a mortgage is too expensive”

Although it’s true that monthly mortgage payments can be expensive, depending on where you live, it might actually be cheaper to buy than to rent.

According to a report from Zumper, the national median rent for a one-bedroom apartment is $1,217. The more in-demand, the higher the price — for example, the median rent for a one bedroom in San Francisco, CA and a one bedroom in New York, NY are $3,500 and $3,000, respectively.

By comparison, the national median monthly mortgage payment is $1,017, as reported in the latest American Housing Survey from the U.S. Census Bureau.

There’s also the matter of home equity to consider. Every time you make a mortgage payment, you reduce the amount you owe on your home while simultaneously increasing its value. Essentially, the more you put into your home, the more you get out of it — and, if you intend to sell your home in the future, you could see significant returns.

On top of monthly payments and home equity, there are tax deductions for homeowners that you might qualify for and take advantage of once your purchase your home.

Still asking yourself if you should buy a home or continue renting a home? There are plenty of free calculators that can help you run the numbers!

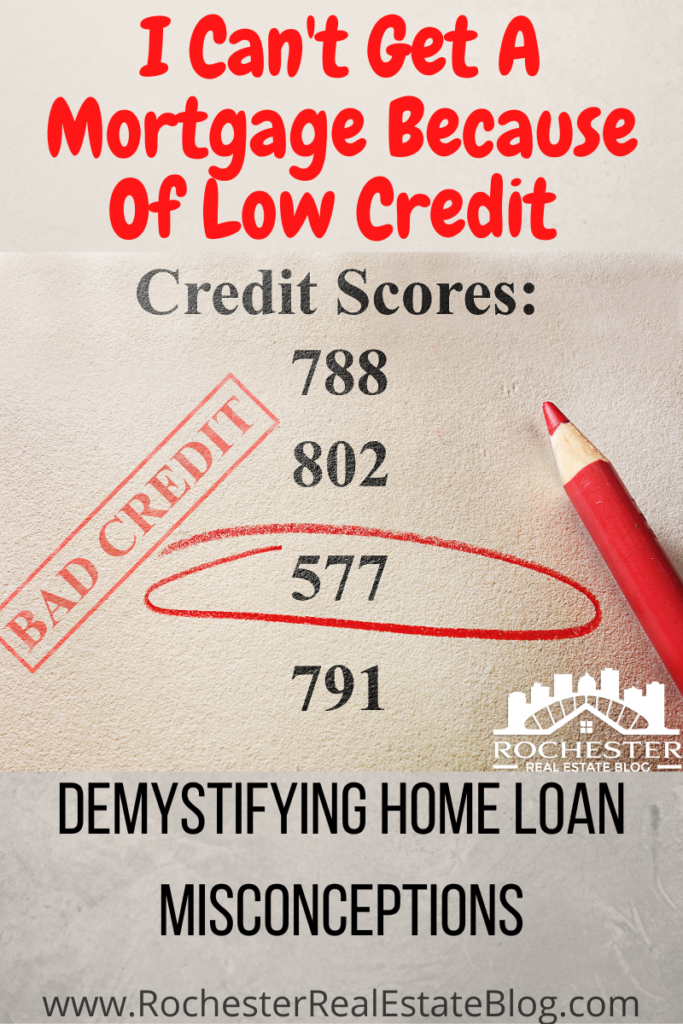

“My credit score is too low to qualify”

A low credit score isn’t necessarily a barrier to becoming a homeowner. If you’re not sure what your credit score is, there are plenty of free tools that can give you an idea what your score is, including Credit Karma. Here is an excellent guide to explaining what is Credit Karma and how it works!

Although there are certainly benefits to having a credit score that falls into the 740 and higher range, most loan types include a fairly reasonable minimum credit score, and some even cater specifically to borrowers with low credits scores.

To illustrate the point, most lenders will accept a credit score as low as 640 for a USDA loan, and a score as low as 620 for a conventional or Veterans Affairs (VA) loan. If your credit score falls below this threshold, you might still qualify for a Federal Housing Administration (FHA) loan, which allows for a minimum credit score of 500.

If your credit score falls below this threshold, you might still qualify for an FHA loan: Home buyers with a credit score of between 500 and 579 are eligible for an FHA loan with maximum financing of 10% down, whereas buyers with a credit score of 580 or higher are eligible for maximum financing of 3.5% down.

“I haven’t set aside enough money for a down payment”

That’s OK because there are plenty of ways to buy a home with little or no money including low to zero-down payment loans. It’s possible to get a conventional loan for as little as 3% down, and an FHA loan for 3.5% down, provided you have a credit score of 580 or higher.

If you’re thinking about buying a rural home, you might qualify for a United States Department of Agriculture (USDA) loan, and if you’re an active-duty service member, a veteran, or are the spouse of a service member, you might qualify for a VA loan — both of which offer $0 down payment options.

It’s also possible to put a monetary gift toward your down payment, though different types of loans have different restrictions around who qualifies as an acceptable donor. For example, FHA loans allow for monetary gifts from family, a fiancé or domestic partner, and friends (so long as the relationship is clearly defined).

As you can see, no down payment mortgages, or very low down payment mortgages, can be found!

“I can’t afford to hire a Realtor”

Although you technically don’t need a Realtor in order to buy home, partnering with one will save you a lot of frustration in the long run. There are way more good reasons to hire a buyers agent when buying a home than doing it on your own!

There are too many horror stories of would-be home buyers who decided to go at it alone, only to spend thousands more than necessary because they were unable to perform a comparable sales analysis on their own.

All of this is to say that yes, hiring a Realtor can be expensive, but it’s almost certainly less expensive than going through the home buying process on your own.

If Realtor-related costs are a concern to you, it might be comforting to learn that the seller typically pays the real estate agent’s commission, as well as Realtor fees.

“I’ve applied for a mortgage in the past and was denied”

There are many reasons a home buyer is denied for a mortgage. It can be a rattling experience, but it shouldn’t take you out of the game completely. To set yourself up for success the next time you apply for a home loan, start by looking at the reasons you were denied.

Was it due to a low credit score? There are a number of great ways to boost your FICO score for a better home loan, including limiting your credit card usage, making consistent payments and working to maintain a credit card balance lower than 30% of your available credit.

Was it because you have a high debt-to-income (DTI) ratio. Before you reapply, work toward paying down your debt so that your DTI doesn’t exceed 36%.

Was your denial because you had insufficient income or asset documentation? Be sure to keep a detailed record of your finances and assets, document all of your income and prepare your tax returns from the past few years so that next time, nothing is omitted.

These are just a few examples of the ways in which you can learn from the mistakes of the past in order to ensure a bright future for yourself — one that includes homeownership.

Final Thoughts

We hope this article has helped you realize that just because you may be down, doesn’t mean you’re completely out.

These common home loan misconceptions don’t have to be the reasons you don’t try to purchase a home!

Despite the odds, with the right approach and loan type you, too, can qualify for a home loan.

Other Home Buying & Mortgage Resources

- 13 Tips To Help You Prepare For Getting A Home Loan via Petra Norris

- 14 Step MEGA Guide To Buying A Home

- 3 Creative Ways To Improve Your Credit Score via Paul Sian

- Don’t Blow Up Your Home Sale – 8 Ways To Ruin Your Home Financing via Michelle Gibson

About The Author: This article “Top Mortgage Myths | Demystifying Common Home Loan Misconceptions” was written by Roger Odoardi. Roger is a co-founder, partner and licensed mortgage broker at Blue Water Mortgage Corporation, an independent mortgage broker serving Massachusetts, New Hampshire, Maine, Connecticut and Florida with 20-plus years of experience in the financial services industry.

About Rochester’s Real Estate Blog: Rochester’s Real Estate Blog is owned and operated by Kyle Hiscock of the Hiscock Sold Team at RE/MAX Realty Group. With over 40 years combined experience, if you’re thinking of selling or buying, we’d love to share our knowledge and expertise.

We service the following Greater Rochester NY areas: Irondequoit, Webster, Penfield, Pittsford, Fairport, Brighton, Greece, Gates, Hilton, Brockport, Mendon, Henrietta, Perinton, Churchville, Scottsville, East Rochester, Rush, Honeoye Falls, Chili, and Victor NY.